Most brands don’t get disrupted because they “lost brand”. They get disrupted because their portfolio math breaks: the entry line attracts the wrong customer, icons stop compounding repeat, and the top end becomes a showroom instead of a margin engine. When those layers drift, you don’t just lose revenue — you lose pricing power, cash flow stability, and your ability to scale without leaning on promos.

A quick story you’ll recognize

Imagine a luxury brand doing ~$60M. The CEO thinks the problem is “top-of-funnel.” The CMO thinks it’s “creative fatigue.” Finance thinks it’s “margin compression.”

They launch an entry product to widen acquisition. It works — CAC looks great, orders spike, management celebrates. Three months later the reality shows up:

Return rates creep up on the entry SKU.

Email performance drops because the list is now full of low-intent buyers.

Icons start getting discounted more often to “hit monthly targets.”

Contribution margin shrinks even though revenue is up.

Nothing is “broken” in isolation. The portfolio is misaligned. The brand is now acquiring customers who behave like shoppers, not fans — and the whole system starts bending around them.

The portfolio model (and why it’s so hard to copy)

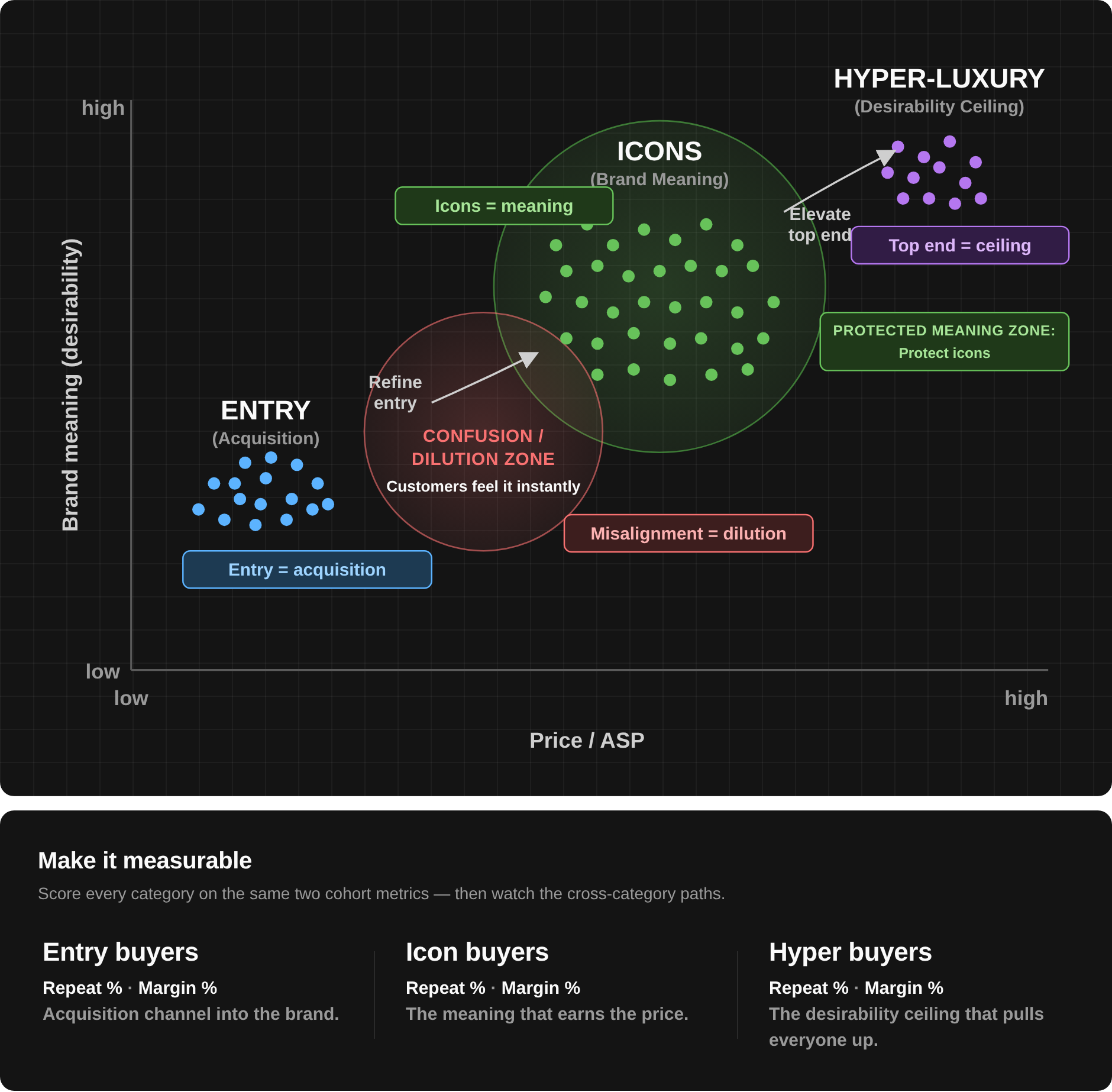

Luxury isn’t one business. It’s three businesses inside one brand:

Icons protect meaning and create repeat. They’re the backbone of trust.

Entry feeds acquisition. It’s the “front door” into your customer file.

Top end maintains the ceiling of desirability. It’s where margin and halo should live.

Luxury Portfolio

The best luxury strategy is a portfolio.

Protect icons, refine entry, and elevate the top end — three categories, three jobs, one brand.

When these layers work together, you get a compounding flywheel: entry introduces, icons convert to repeat, top end upgrades the best customers and strengthens the brand’s “why.”

When they’re misaligned, customers feel confusion immediately. You see it as: promo pressure, softer repeat, diluted positioning, and a customer file that gets worse over time.

4 principles that change how you operate

Your entry line is not a revenue line — it’s a customer quality filter

Entry products decide who you attract: bargain hunters, gift buyers, true category fans, or “deal tourists.” If entry is over-indexed on discounting or low perceived value, you’re manufacturing a future retention problem.

Icons are your retention engine, not your bestseller shelf

Icons aren’t “products that sell a lot.” Icons are products that retain the right customers and create predictable repeat. If you don’t measure icon performance by cohort behavior, you’ll end up protecting the wrong SKUs.

Hyper-luxury is not about volume – it’s about maintaining the ceiling

Top end works when it upgrades your best buyers and keeps your brand’s desirability credible. If it’s disconnected from the customer journey (no upgrade path, no cross-category pull), it becomes a vanity line that eats attention without compounding LTV.

Portfolio misalignment shows up as margin chaos before it shows up as brand chaos

The first symptom is rarely “we’re losing relevance.” It’s usually: higher returns, lower repeat rate, weaker full-price conversion, and more dependence on discounting to move inventory. That’s not marketing — that’s portfolio economics.

|

✓

|

|

The Operator Playbook

|

| What to do next |

| Five portfolio moves to turn your assortment into a capital allocation system. |

|

|

|

|

Segment your customer file by the product that acquired them.

For your top 20 acquisition SKUs, build a simple view:

| • |

12-month LTV (or CM1 LTV) |

| • |

Repeat purchase rate |

| • |

Return rate |

| • |

Cross-category paths (what they buy next) |

This instantly tells you which entry products create fans vs one-and-done shoppers.

|

|

|

Define “icon” with behavior, not taste.

Pick your icon candidates, then validate with data:

| • |

Do buyers of this product have higher repeat? |

| • |

Do they expand into other categories? |

| • |

Do they require less discounting over time? |

If a so-called icon doesn’t improve cohort health, it’s not an icon — it’s just famous.

|

|

|

Build an upgrade path: entry → icon → top end.

Most brands have products. Few have progression. Create intentional bridges:

| • |

Bundles that move entry buyers into icon formats |

| • |

Post-purchase flows that educate and elevate — not just “10% off next order” |

| • |

Merchandising that surfaces “the next best product” based on affinity |

Luxury scaling isn’t about more drops — it’s about better customer journeys.

|

|

|

Protect the portfolio with rules, not vibes.

Set guardrails that finance and marketing both respect:

| • |

Promo eligibility by segment — VIPs shouldn’t be trained to wait |

| • |

Discount limits on icons — protect meaning and margin |

| • |

Entry products you advertise — only those that create high-quality cohorts |

This is how you stop “growth” from quietly turning into dilution.

|

|

|

Run a monthly portfolio review like a CFO, not a creative director.

Your portfolio is a capital allocation system. One meeting. One dashboard. No debates.

| • |

Which entry SKUs improved customer quality this month? |

| • |

Which icons are compounding repeat? |

| • |

Which top-end products are upgrading customers vs just existing? |

|

|

|

BOOK YOUR AUDIT →

|

|

Why this is hard without a real intelligence layer

Most brands can’t answer the portfolio questions because their data is trapped in channel dashboards and SKU-level sales reports.

You need to see who is buying, what they start with, and how they behave over time — by cohort, by segment, by product path, and by margin. That’s the difference between “taste-based strategy” and measurable portfolio strategy.

RetentionX makes the layers measurable: icon buyers vs entry buyers vs hyper-luxury buyers, their repeat purchase rate, cross-category paths, and margin by cohort — so you can tighten the product mix without guessing where desirability turns into dilution.

The simple summary

Brands don’t scale by being louder. They scale by building a portfolio where entry acquires the right customers, icons compound repeat, and top end preserves the ceiling. When those layers are aligned, you get stable cash flow, stronger LTV, and growth that doesn’t require constant promotions.

If you want a sanity check on your own portfolio — which SKUs are acting as entry, which are true icons, and whether your top end is actually upgrading customers — check our Audit offer.

|

Reader questions

|

| Ask me anything. |

| Smart questions from operators in my inbox — my honest answers. |

|

|

What’s the most common misalignment you see in practice — entry product drifting too promo/price-led, icons getting over-extended, or the top end not being “visible” enough to maintain the ceiling? |

|

|

|

|

Alex says · Founder RetentionX |

|

| Most often it’s entry drifting into “discount acquisition,” which changes who you attract and what they expect. The second is icon over-extension — too many variants, too many collabs, too much availability — until it stops feeling like an icon. And sometimes the top end exists but isn’t strategically used, so the ceiling of desirability isn’t actually doing its job. The portfolio works when each layer has a clear role and you protect the edges from leaking into each other. |

|

|

|

How do you measure “desirability dilution” early, before revenue shows it? Do you use repeat rate + return rate + discount depth, or are there better leading indicators (e.g., full-price share, time-to-second-order, cross-category progression)? |

|

|

|

|

Alex says · Founder RetentionX |

|

| A mix of economics and behavior: full-price share, discount depth on repeats, return rate, and repeat purchase rate by cohort segment (entry vs icon vs top end). The early warning sign is when entry buyers stop progressing up the ladder and instead repeat only under promo — or churn entirely. Cross-category paths matter a lot: healthy luxury files show a pattern of “entry → icon → adjacent icon,” not “entry → discount loop.” If that ladder breaks, dilution usually follows. |

|

|

|

|

|

|

Alex says · Founder RetentionX |

|

| No — entry only helps when it’s a controlled on-ramp to your real margin and meaning. If entry attracts buyers who never trade up, you’ve built a separate business that can dilute the brand and pull ops toward volume. The test is simple: do entry cohorts show progression (second purchase, cross-category movement, rising CM1) and do they behave closer to your best customers over time? If not, entry is just discounted acquisition wearing a luxury label. |

|

|

|

In luxury, a lot of the “portfolio” lives across channels (boutiques, wholesale, marketplaces). How do you handle cohort measurement when part of the purchase behavior is off-platform and identity is fragmented? |

|

|

|

|

Alex says · Founder RetentionX |

|

| You won’t get perfect identity everywhere, but you can still make better decisions by stitching what you can and reconciling the rest at the contribution level. Start with the channels where you have first-party identity (DTC, loyalty, clienteling) and build cohort curves there. Then use proxies for off-platform: SKU/channel-level repeat signals, return/discount patterns, and customer migration (e.g., DTC buyers later buying in-store if you can capture it). The goal isn’t perfect omnichannel attribution — it’s identifying which portfolio layers create healthy customers vs noisy volume. |

|

|

|

When icons are doing the heavy lifting, how do you prevent the brand from becoming overly dependent on them? Is the move to ladder entry → icon, or to create “adjacent icons” and track whether they actually create similar repeat/margin behavior? |

|

|

|

|

Alex says · Founder RetentionX |

|

| Both, but in the right order. First, make sure entry reliably ladders into icons — otherwise you’re building a low-quality base that doesn’t feed the core. Then you expand with “adjacent icons,” but you validate them the same way you validate the original: do they create similar repeat patterns, cross-sell behavior, and margin by cohort? If they don’t, they’re just incremental SKUs, not portfolio builders. Dependency risk goes down when you have multiple products that create the same type of customer — not just more products. |

|

|

Listen on Spotify

Listen on Spotify